Condo Economics.

And why we like condos as an investment opportunity in this part of the cycle.

Why do we think ground-up development of for-sale luxury residential is the best real estate investment at this moment of the cycle?

Over the past few months, we’ve heard from many real estate investors who are avoiding new commitments while they wait for interest rates and market direction to stabilize.

Meanwhile, we have doubled down on our thesis that ground-up development of for-sale luxury residential projects presents a compelling opportunity that's being largely overlooked.

At first glance, this may seem counterintuitive. Development is widely viewed as the riskiest corner of real estate, especially in an environment of elevated interest rates and economic uncertainty. But when we dig deeper into certain geographies and market segments, a different picture emerges, where development margins of ~35% are achievable using today's prices, with no need to bet on future appreciation.

Development economics differ from traditional real estate investments. Rather than betting on cap rate compression or NOI growth over a hold period, development creates value through the design, construction, and sales processes.

This approach is even more compelling when three market conditions are present: normalized land prices post-ZIRP, construction financing structures that limit exposure to rate volatility, and buyer demographics that rely on cash rather than financing.

When these factors exist in markets with significant wealth concentration, the result is an investment structure that operates largely independent of the macro forces currently affecting other real estate sectors.

Here’s how we think of these factors in greater detail:

1 - Deals pencil with no forecast price appreciation.

Even using today’s sellout prices (prices on real sales from 2025 and 2024), we can underwrite development margins of ~35% for luxury condominiums in many major metro (and some resort town) markets.

(Defect laws and other local regulations may limit condo development in some jurisdictions, but for the purpose of this description, we will consider that a separate factor, and we will address those risks at the end of this newsletter.)

What is a development margin?

It's the project profit/project cost. A 35% margin is slightly better than building to an 8% yield on a cost in a market where your building can be sold at a 6% cap rate.

Said another way, today’s sellout prices could fall by 35%, and a project would still break even before fees.

In ground-up development, the economic return is created through the development process, not through cap rate compression or assumed NOI growth.

In most real estate markets that are priced on cap rates, there are two ways to make a profit investing in real estate:

1. EITHER

The NOI goes up. This could be “forced” through improvements in operations, raising rents to market, improving the quality of units to capture a higher rental rate, etc, or through annual rent growth over time in markets that exhibit favorable supply/demand imbalances (lots of demand, not too much supply).

2. OR

Cap rates can move down. Maybe because there is more money chasing the same fixed inventory of assets, or positive investor sentiment is reducing risk premium everywhere, or because interest rates are low. For example, when cap rates move from 6% to 5%, the existing NOI is valued at a higher multiple.

The above can be amplified – in both directions – by using leverage. (More on this dynamic in #4 below).

In ground-up and conversions, the returns do not come from “growing” income (increasing NOI) or from expecting that income to be more valuable (cap rate compression). They come from changing the use of the land or the existing building into something more valuable and then selling that something more valuable at today’s prices (or hopefully higher, but importantly not required to be higher).

Development math is simple:

$100 land cost

$200 cost of improvements i.e. construction + soft costs

$50 interest cost on the construction loan

$475 sales price

This type of business plan doesn’t rely on rent growth, cap rate compression, or on “improving operations with the use of technology.”

2 - Interest rate volatility has a limited impact on returns because interest on construction loans is the only direct interest rate component, and typical construction loans are only 2-3 years with an average balance outstanding of only 50% of the total balance.

When you buy an apartment building at a 6% going in cap rate (NOI is 6% of purchase price), with a 5-year 6.5% fixed rate loan at 80% LTV loan, a few things happen.

After the tenants pay their rent, and you pay your expenses, including your interest expense, you have a little bit of money left over.

In this case, it happens to be 4% of your equity investment every year (4% cash on cash return). If that loan rate falls just 1% to 5.5%, you suddenly have twice as much net income on your investment, and you go from a 4% CoC return to an 8% CoC.

What do you think happens if instead of going down 100bps, the loan rate goes UP 100bps?

Yup, you guessed it.

Now you have a 0% CoC return.

What if the rate goes up another 100bps?

Yikes, now you LOSE 4% of your equity every year (and that cash must come from somewhere, so you have a capital call to look forward to as well).

These differences in loan rates are magnified the longer you hold an investment – a year or 2 losing 4%/year is survivable. A decade of losing 4%/year is disastrous.

In development, the impact of changes in loan rates is different.

In a project with a 24-month construction timeline, a construction loan interest rate of 8%, and a pre-sale volume of 30% (30% of units are sold when Certificate of Occupancy is delivered), total interest expense is only 8-10% of maximum construction loan balance, which is only about 1 year of interest on the full loan amount.

How can that be?

The outstanding construction loan balance increases slowly from 0 to the full amount over the entire course of construction.

The increase isn’t linear, and most of it occurs in the later phases of construction, since every month your loan balance increases as you process loan draws to pay for construction. Once you have a CO and your presales close, those sales proceeds are first used to pay off the construction loan.

If there is any leftover, LPs receive a check for return of capital.

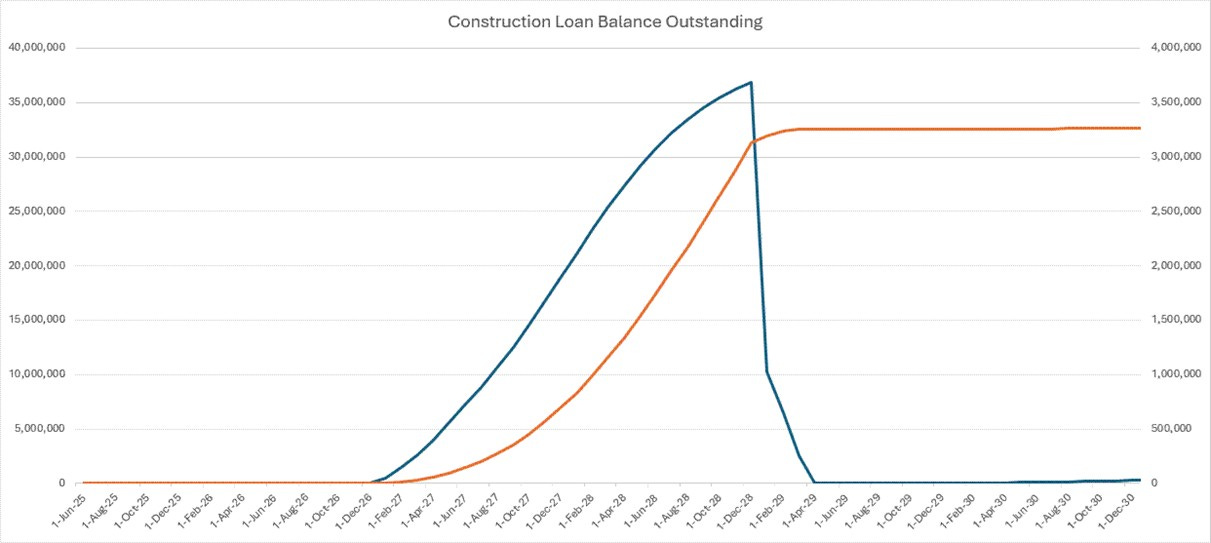

In the chart below, you can see the typical progression of the construction loan balance from site acquisition, through pre-dev, into construction, and finally into presales and sales.

This means that construction loan interest typically represents about 5-6% of total construction cost, and about 13-17% of profits.

Of course, a developer should do everything they can to move a project along quickly to minimize interest costs, but a change of 1% of even 2% in interest rate will not move a project from profitable to unprofitable, unlike in other RE sectors, where a 200bp swing in interest rates can be the difference between earning a positive return or losing most of your investment.

Blue Line: construction loan balance outstanding

Orange line: total interest paid

3 - For-sale condo product provides a relatively quick return of capital and profit with no hold vs sell decision.

There has been a lot of discussion in the last 5-10 years about “holding forever”. We’ve seen it not only in real estate but also in other asset sectors.

However, if the last few years have taught us anything, it’s that ”forever” has turned out to be a poor investment if the real intention wasn’t actually decades-long.

Since peak “forever,” cap rates have expanded as much as ~200bps depending on the asset class and geography, destroying a lot of value (sometimes all of the value) in real estate investments.

Not all investors can afford to stay invested through generations.

In for-sale luxury development projects, the building gets sold, one unit at a time.

There is no controlling LP or GP keeping capital trapped inside a deal, and there is no value destruction from an increase in cap rates or interest rates 5 to 15 years after purchase.

Instead, in major metro areas with diverse demand and a high concentration of wealth, there is a steady return of capital and profits until the last unit is delivered, and a project is closed out.

Note: If unit sales are not achieving price expectations, the developer typically has the option to rent some of the units until demand returns to sufficient levels. This is one way to mitigate losses – and preserve LP equity – when sellout expectations are not initially met.

This would be a worst-case scenario, where other mitigating measures were either not considered, or weren’t successful. We discuss some of our risk-mitigating strategies for the NY condo market here.

4 - Changes in cap rates do not impact value, because sellout is based on the market price per square foot, and cost is a function of land value + construction costs.

When you buy a cash-flowing real estate asset, you are buying an income stream created by tenants paying their monthly rent. As discussed in section #2 above, this income stream is valued on a cap rate basis (the NOI multiple that is the inverse of the cap rate).

Buying a deal at a 5% cap rate?

You’re paying 20x NOI.

A 6% cap rate? 16.66x NOI.

7%? 14.3x NOI.

(You get the idea.)

The point is, when the cap rate changes (driven by changes in interest rates, the stock market, or the underlying economy), the value of your cash flow and the value of your real estate investment also change.

This can be great when interest rates are falling, the economy is strong, and the stock market is booming, which is a highly unusual occurrence.

Usually, when the economy and stock market are both strong, interest rates actually rise, putting upward pressure on cap rates that are typically offset by robust expected NOI growth due to a strong economy and increased investor optimism .

As we have seen in the last several years, this highly unusual occurrence was abruptly reversed when interest rates spiked, causing both the real economy and the stock market to retreat.

Investors, real estate or otherwise, predictably followed suit and became more cautious. Hence, cap rates expanded dramatically, evaporating lots of equity.

The point is this: when you invest in an income-producing real estate asset, especially one that is remaining largely as-is after purchase, you are inherently betting on cap rates.

5 - The high-end market segment is less sensitive to short-term economic fluctuations, interest rates, and the stock market.

The spending habits of the wealthy tend to differ from those of the average person.

Not only do they spend on different things, but they 1) have far more disposable income 2) their savings rates are far higher, 3) they have significantly less debt as a proportion of income and assets, and 4) they only borrow money because they choose to, not because they have to.

As an example, all-cash condo buyers in Manhattan represented over 70% of all buyers in 2024, and even in periods of low interest rates, all-cash buyers tended to account for 60% of transactions or more.

The aggregate US savings rate, as a % of disposable income, is about 5%. Over time, it tends to fluctuate between 5% and 6%. The savings rate for the top 10% to 1% is about 12%. And the savings rate for the top 1% is 38%.

People who save 38% of their income every year can withstand a significant decrease in income before their spending habits start to change.

All these factors contribute to more consistent spending patterns that are much harder to disrupt than those of the average or even above-average consumer.

These buyers are not selling their stock portfolios to fund down payments and are not reliant on the mortgage market to fund purchases. They have cash at hand (and cash equivalents like money markets or T-bills), and they simply use that cash to buy properties. This creates a very beneficial dynamic for real estate developers who build the high-end products these buyers desire, and in favorable, high-demand areas, these buyers show up rain, shine, recession, or bond market sell-off.

6 – The “free money” era is over, which means land values now support profitable development projects with reasonable underwriting assumptions.

The ZIRP era is over. The federal funds rate is at 4.35%, down from a peak of 5.35%, after spending most of 2020 and 2021 near 0%. When the base borrowing rate in the economy approaches 0% and stays there for an extended period, many economic anomalies begin to occur.

One of those anomalies is that any project with a positive NPV (net present value) becomes attractive to capital that would otherwise sit in a bank account earning a 0% nominal return (and a profoundly negative real return after considering realized inflation).

And what better way to create a positive NPV than by investing in or building real estate?

The extended period of ~0% interest rates caused many projects to be pursued – ground up, value add, or otherwise – that frankly would not or should not have been built under any other circumstances.

And because capital was willing to chase any return, inexperienced or otherwise unqualified operators could attract that capital on a highly unusual scale.

That era has been over for a few years.

What does this mean for developers pursuing site acquisitions today?

It means we are no longer competing with so many inexperienced teams for development sites. We are mainly competing with other established developers who understand underwriting, construction costs, and sellout prices.

This means that, in general, investment sales prices have normalized, and it is possible to acquire development sites at a price that will likely generate very attractive risk-adjusted returns for investors.

So why is development considered "so risky"?

The perception comes from four primary risk factors: entitlement, construction, sales, and defect laws. These are real risks that have caused problems for many projects and operators.

The difference is that these risks are execution risks that experienced operators can control through proper due diligence and conservative underwriting. This is unlike the macro forces that drive cap rates and NOI growth, which are completely outside an investor's control.

The current environment works in favor of experienced developers.

Land prices have normalized, competition from inexperienced operators has decreased, and the wealthy customer base remains largely unaffected by broader economic volatility. For operators who understand the development process, the risk-adjusted returns available today are attractive.

In our next newsletter, we'll examine each of these four risk factors and explain how experienced developers mitigate them. We'll also look at why the development process might actually carry less risk than many traditional real estate investments when executed properly.

For us, the question isn't whether development involves risk. It's whether the returns justify those risks, and whether you have the right team to manage them effectively.

If you are interested in investing in our fund, let us know via the investor interest form below.

AND

We are looking for long-term capital partners interested in a 5 to 10-year hold and looking for investment opportunities in the $10-$50mm range.

OR

If you have a development site with at least 40,000 buildable square feet zoned for residential use as of right in Manhattan or a good candidate for an office-to-residential conversion, let us know!

Most importantly, we want to meet and begin building relationships with people who are interested in what we are doing and who believe in how we approach the work, regardless of interest in our current deals.

Send us a note if you’d like to chat!

In addition to our development work in NY, MADDPROJECT provides fee development and professional project management services across the US.

Need help and don’t know where to start?

Have a specific subject you want to see us tackle in a future Newsletter?

Drop us a note!

| A guest post by

|